In this 13 minute video, Lydia Wietsma and I discuss the most recent five things you need to know about forbearance. The majority of borrowers leaving forbearance are current upon plan exit, only 13% of borrowers leaving their forbearance plan do so without having a loss mitigation plan in place. There is not much time left if someone needs to take advantage of these CARES Act benefits.

We do these updates to help real estate professionals and consumers understand forbearance, and to let struggling borrowers know that although experts are forecasting a tough winter, there are options.

One.

Last week total number of mortgage loans now in forbearance increased slightly from 5.48% to 5.49% as of December 13, 2020. According to MBA’s estimate, 2.7 million homeowners are in forbearance plans.

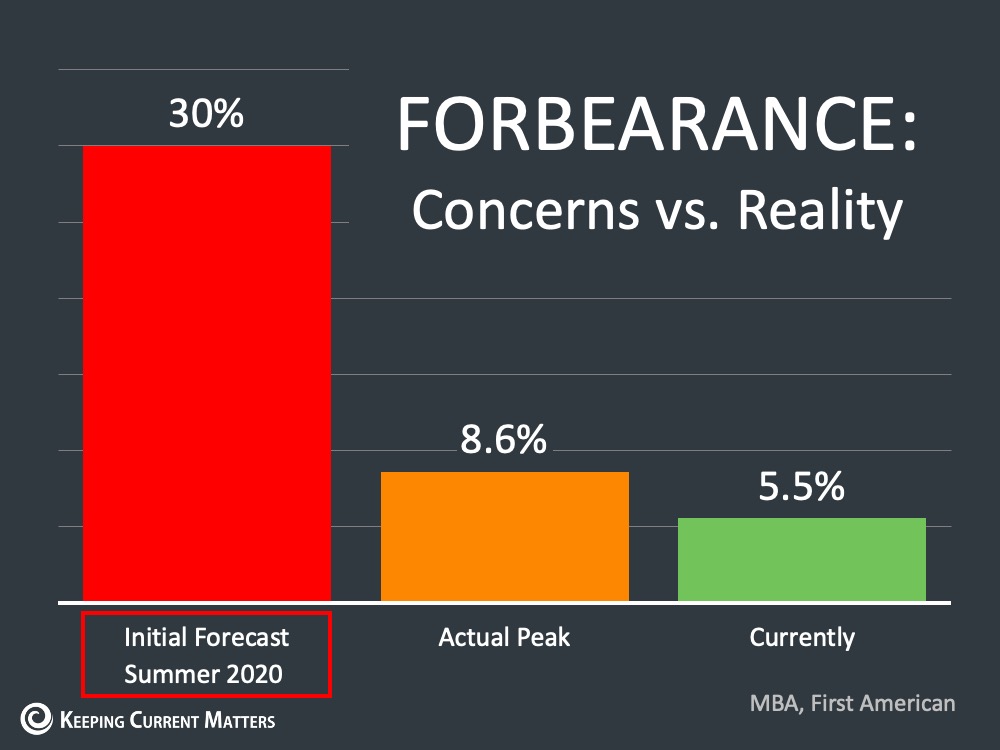

While the news of an increase is not great, we need to remember total loans in forbearance was expected to hit 30% and our peak was 8.6%.

Two.

Forbearance Numbers by Stage:

- 18.78% of total loans in forbearance are in the initial forbearance plan stage, which is up very slightly from the previous week which was 18.72%.

- 78.54% are in a forbearance extension, this is down from the previous week which had 78.72% in extension.

- 2.69% are forbearance re-entries which is up from the previous week of 2.56%. This group has been slowly growing over the past few weeks.

About 13% of the borrowers exiting forbearance are still behind on their payments and left their program without a loss mitigation plan in place. This is the group that needs to know their options.

When you look at this slide, this means that we are looking at roughly 116,000 borrowers in this situation who will need guidance.

Three.

While the new stimulus bill covers renters, landlords, extends the PPP loan options for small businesses, extended unemployment benefits, and more, it does not extend forbearance plan protections.

Eviction and foreclosure protections were extended through 1/31/2021.

Four.

Borrowers who want to get started in a forbearance plan have 4.5 business left to call their servicer to get started. Time is of the essence.

Five.

Lydia is receiving more and more inspection requests from the servicer she works with. So far this week she has received 10 requests. The activity is picking up.

When exiting forbearance borrowers have a number of options; not all of them require the owner to sell their property. Some of these options include:

- Utilizing a 401K in two ways.

- Individuals are allowed to borrow from their 401K with the option of paying themselves back with interest, since it is a loan being paid back, essentially paying yourself back there are no penalties. Talk to your 401K administrator for details.

- Through provisions of the CARES act, an individual can also withdraw an amount of their 401K with no penalties. Again, talk to your 401K administrator for details.

- Permanent loan modification or refinance, after making 3 payments in a row, to something that allows borrowers to stay. Some scenarios include adding the forborne amount at the end of the loan, some pay a lump sum to get caught up, some offer payment plans to get caught back up.

- Rentals are in high demand with quickly appreciating values. What about moving out of the property and renting it out to make up the difference in payments.

- Sell and buy something more affordable, after 3 payments in a row have been made. Pay off the loan and get a new loan with more agreeable terms.

- Sell, pay off the loan and forborne the amount, and rent/move in with family.

Sarah Perkins is an award winning account executive and has been in title sales since 2004. As the Director of Industry Research & Senior Account Executive, Sarah’s role is to bring real estate transactions to Navi Title. Sarah supports her clients by helping them navigate the ever-changing real estate space through thorough research and understanding of current trends impacting today’s home buyers and sellers.