Yesterday I had lunch with three of Greater Phoenix’s premier real estate analysts. As the conversation moved from appreciation rates to price reductions to data quality to seasonality, the question kept coming up, “What do you think will happen in 2022?” It is forecast season after all. Time to reflect on the year that was and plan for the year ahead.

Before I go further, I am pleased to announce that I recently joined Clear Title. While remaining in the sales arena, I will use my research on the real estate industry to solve specific client challenges. The best way I can support our clients is by understanding their business and the subtle nuances and shifts within the real estate space. Click here for the Phoenix Business Journal announcement. Click here for the Clear Title press release.

National Real Estate:

Despite significant headwinds, at over 6.2 million, 2021 is on pace to have the most existing home sales since 2006.

“Home sales remain resilient, despite low inventory and increasing affordability challenges. Inflationary pressures, such as fast-rising rents and increasing consumer prices, may have some prospective buyers seeking the protection of a fixed, consistent mortgage payment.”

-Dr. Lawrence Yun, Chief Economist for NAR

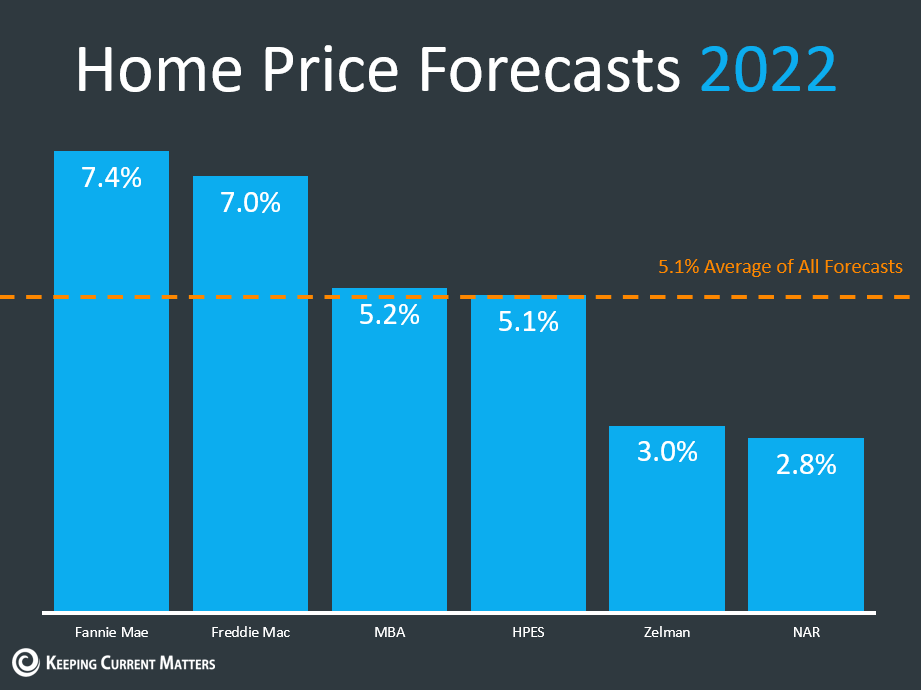

Fannie Mae projects that we will see declining sales volumes over the next two years. If 2021 has the most sales in the past 15 years, then it only makes sense that there would be fewer sales in the next two years. Even still, the 2022 and 2023 projections both call for sales volumes greater than every year from 2007 through 2018.

The headlines look bad but the actual numbers show continued growth and stability. Fannie Mae, despite the negative headlines, forecasts favorable markets for the next two years. While yes, Fannie Mae does predict a downturn in 2023, a lot can happen in two years, just look at the past two years. No one predicted any of it. That 2023 prediction is based on seasonal trends going back 60 years. While some elements of seasonality have emerged over the past six months, it is muted and unpredictable. Inventory is declining faster than normal and demand, particularly luxury demand, remains strong, which is also unusual for Q4.

Inventory:

With inventory declining quickly, we may start 2022 with fewer homes on the market than we had at the beginning of 2021. If inventory stays low, prices will continue increasing. If inventory increases, then prices will rise more slowly. There is a lot of speculation that supply will rise, but the question remains, by how much and when?

Appreciation & Inflation:

When we are in a balanced market, homes appreciate at the rate of inflation. Today, that means homes would appreciate at 6.2%. The forecasts that call for appreciation rates under 6% are essentially calling for negative appreciation. In 2022, Realtor.com expects a 3.6% appreciation rate and Forbes expects a 16% appreciation rate. With ranges this wide, how educated are these guesses, I mean forecasts?

The AZ Market:

2021 will likely turn out to be Greater Phoenix’s biggest resale year by units, outpacing even 2005.

In January 2020 all signs pointed to a year with 10-12% appreciation. I was concerned about the lack of sustainability of appreciation rates that high. Little did I know that 2020 would end at 18% appreciation and continue growing. In April we hit 4% month over month appreciation and by June we dropped to only a 1.1% appreciation rate month over month.

In July and August, when the median sales price stayed flat month over month at $405,000, we thought we would see some real normalization. The median sales price in November was $420,000 giving us an appreciation rate of 28%!! Back to back years with appreciation rates this high is unsustainable and unhealthy for the overall market.

Tapering:

The Federal Reserve may speed up its bond and mortgage backed security purchase tapering. The persistently high inflation is not abating meaning that the Fed expects to raise rates sooner than expected. The tapering is currently expected to be complete by June 2022 but the timelines may move up to a March 2022 completion date in order to raise rates as early as April 2022. Some say June was too cautious and others are concerned about demand declines if we have another “tamper tantrum” like in 2013 when sales declined by 10%, appreciation slowed but did not go negative.

Real Estate News:

- Several law firms are investigating Zillow for potential securities fraud, which is not uncommon when a company pivots and share prices drop significantly. In only a few weeks Zillow’s market cap has dropped from $21.3 billion to $14 billion.

- At the end of 2020 NAR had $50M in reserves. By the end of 2021 NAR expects to have $160M in operating reserves and $91M for advocacy reserves. The increase is to help fund the DOJ lawsuits battles.

- People with a net worth of $5M+ own an average of $1M-$5M in real estate. That is a 180% increase from 2019.

- Opendoor, Offerpad, Zillow sold 20% of their inventory to investors this year. This week three Senators requested information from Zillow on how many homes the company has sold and plans to sell to Wall Street firms.

- The elimination of 1031 exchanges was removed from the recently passed infrastructure bill.

- The conforming loan limits are increasing more than initially expected, at an 18% increase the new limit is $647,200 for conventional financing.

Final Thoughts:

As our lunch ended yesterday, we agreed, that with so many different moving parts – many operating outside of typical seasonal trends – it is extremely difficult to comfortably forecast anything past Q1 2022. We agreed that 28% appreciation is unsustainable, and it is unlikely that we will see appreciation at even half that rate next year. After 2020’s 18% appreciation and 2021’s potential 28%+, an appreciation rate of 8% to 10% for 2022 would be welcomed by buyers and would ultimately put us on a better path towards a healthier real estate market.

Copyright 2021 Sarah Perkins

Sarah Perkins is an award winning account executive and has been in title sales since 2004. As the Director of Industry Research & Senior Account Executive, Sarah’s role is to bring real estate transactions to Navi Title. Sarah supports her clients by helping them navigate the ever-changing real estate space through thorough research and understanding of current trends impacting today’s home buyers and sellers.

Sarah,

CONGRATULATIONS on your new job as Director of Strategic Accounts at Clear Title Agency of Arizona. You are so deserving of this promotion. Well done. I wish you and your family nothing but good health and happiness in 2022.

The appreciation rates over the past two years are staggering! We have witnessed a feeding frenzy over the past two years and it had to end.

David

Thank you David! It is exciting. Yes, the crazy market will calm down and be a bit more manageable.

Sarah rocks!!! She is always willing to go above and beyond for her clients.

Thanks Lance! I really appreciate it!

Congrats Sarah on the new position.

Thanks Matt! I am excited!