Emotions have the ability to cloud our judgment. We are taught to be rational and to only use the facts when making decisions. That sounds good in theory, but when a human is devoid of emotion they cannot make even the simplest of decisions.

Do you have clients still worrying about when the housing market will crash? The intensity of late 2020 and early 2021 felt like the market frenzy of 2005. As the market normalizes it may feel weird or uncomfortable as we pivot again. While those emotions are important and we have to have emotion to make decisions, we have to look at the facts. And the facts point towards stabilization and continued appreciation, just at a slower rate.

National Real Estate:

- Nationwide equity increased by $2.9 trillion since Q2 2020. This translates to an additional $51,500 in equity per borrower over the same time period. Another way to look at it is national negative equity share dropped to 2.3%, the lowest level in 12 years.

- While the extreme price appreciation has benefitted sellers for nearly a year, it is unsustainable. The decline in the rate of appreciation will be noticeable and will feel uncomfortable, however, it is necessary to rebalance the market. Fannie Mae recently released its forecast for the rest of this year and next. I expect to see a 4% to 8% rate of appreciation, year over year in 2022 and Fannie Mae agrees!

- According to Fannie Mae’s most recent Home Purchase Sentiment Index survey, those who said that it is a good time to buy increased by 7 points, month over month, the first improvement in four months. Those who said it was a good time to sell declined by 1 point, month over month in August. Consumers are starting to realize the shifting market.

- Zillow sponsored a recent survey of real estate experts and economists projecting the source of future inventory. The panelists expect to see 40% of listings to come from existing homeowners who are relocating. 23% from home builders. 10% from sellers who plan to rent. And 5% from foreclosed properties. Based on the data above 5% could be a reach.

- After two consecutive months of declines, in August, pending home sales increased 8.1% month over month.

“Rising inventory and moderating price conditions are bringing buyers back to the market. Affordability, however, remains challenging as home price gains are roughly three times wage growth.”

-Dr. Lawrence Yun, NAR’s chief economist

- After two months of gains, existing home sales declined 2% in August, month over month, dropping the seasonally adjusted annual rate of sales to 5.88 million. In 2020 there were 5.64 million home sales.

- National rentals rates are at a 16 year high and up 8.5% year over year in July. In Greater Phoenix rental rates are up 18.9%.

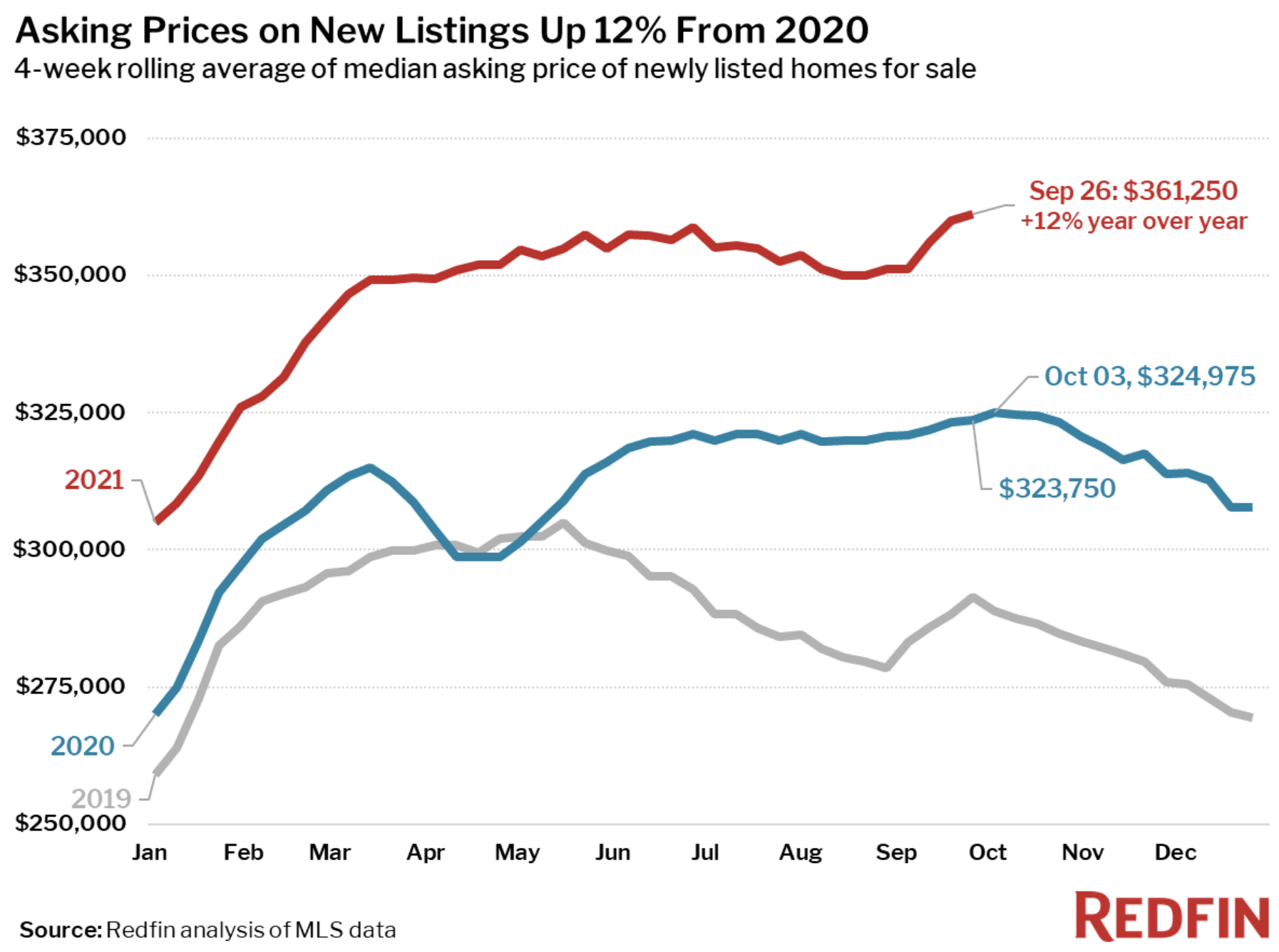

- The median new listing asking price is up 12% year over year and reached a record high of $361,250 for the four-week period ending September 26. For single family only it is $389,900.

The AZ Market:

Demand increased by 11.4% from July 20 to September 30. That is unusual. Demand usually declines in August and September and begins to increase into October as the weather cools. Supply is up 19.6% over the same time period, this is also unusual as inventory tends to decline in the late summer.

Rents are expected to continue increasing. Greater Phoenix rental occupancy is at its highest rate in over 40 years at 97.1%, the highest since 1978.

Since 2016 developers have added 36,000 multi-family units, including leased and build-to-rent properties. 2021 will add 11,000 units, the most since 2009’s 9,315.

Pinal County is growing. In the first half of the year, Coolidge saw a 258% year over year increase in homebuilding permits. In the Town of Maricopa, permits are up 237% year over year.

New home permits are up 25% year over year in August, meanwhile, permits and closings for new single family homes declined for the second month in a row.

Nationally, upwards of 10% of new builds are for build to rent. Phoenix is the third-largest build-to-rent market.

Federal Reserve:

Mortgage rates are increasing. Higher rates = higher monthly payments = decreased affordability. Additional affordability pressure hurts demand. Rule of thumb: one percentage point = $50,000 of buying power.

Whether is it persistent inflationary fears, a strengthening economy, or reaching the debt ceiling, the Federal Reserve announced on September 22 that it expects to begin tapering its $120 billion in monthly purchasing of bonds ($80 billion) and mortgage-backed securities ($40 billion) before the end of the year. The tapering will be complete by Q3 2022.

“Though it may be due to uncertainty arising from brinkmanship on U.S. debt default, I believe it is from the greater recognition of higher inflation. The Federal Reserve has been revising up its inflation forecast and the Fed chairman Powell has changed his narrative to imply as such.”

-Dr. Lawrence Yun, NAR’s chief economist

These monthly purchases that started at the onset of the pandemic to stabilize mortgage rates have grown the Federal Reserve’s debt holdings up to nearly $8 trillion. Remember in April 2020 when jumbo loans all but vanished? It was this action that brought stability and extremely low rates to lending.

The Fed’s hopes to avoid another “Taper Tantrum.” In 2013, when the Fed began tapering its purchases, it only took 8 weeks for interest rates to go from 3.35% on May 2 to 4.46% on June 27 and finally peaking on August 22 at 4.53%. The quick spike in rates caused home sales to decline by 10% and price appreciation slowed but did not go negative.

The Fed’s next meeting is on November 2 and it is expected that the tapering start date will be selected then and could start as early as November. Markets often respond to news and interest rates have been slowly increasing since the September 22 announcement. Once the start date is established expect interest rates to jump as much as a quarter to half a percent. For more, check out my recent discussion from Monday, here.

New Construction:

New home completions were up 4% from July to August. At the same time, single family starts declined for the second month in a row by nearly 3% in August, month over month. New construction will not be the answer to low inventory.

In August, about 80% of new construction sales were either under construction or yet to be built.

Despite that single family construction has been increasing since it bottomed out during the Great Recession, home building is running at the slowest pace since 1995. With a housing unit deficit of 3 to 5 million (depending on the on the data source) it will take many years to close the gap.

Commercial Real Estate:

Sales prices in all four of the commercial real estate sectors are up year over year. 1.) apartments are 14.7%, 2.) industrial is up 13.6%, 3.) retail is up 12.5%, and 4.) office is up 11.2%.

Real Estate News:

- In October 2020 when Opendoor filed it S-4 form with the SEC to go public, it revealed an August 2019 FTC civil investigative demand regarding advertising claims Opendoor made on its website. In its September 15, 2021filing the company warned investors that the deal currently in negotiation may “negatively affect the company’s ability to operate its business” and went on to say, “there are no assurances that we will be successful in negotiating a favorable settlement.”

- In order to combat low inventory and affordability issues, California recently passed a bill that allows, owner occupied, single family properties to be divided into up as many as four units.

- Opendoor partnered with new home search platform, NewHomeSource.com, consumers browsing the site may request a trade-in offer from Opendoor without leaving the search portal.

- Real estate investment company, Groundfloor recently launched a new app called Stairs that allows users to invest in real estate with as little as $1.

- According to Case-Shiller, at 19.7% July had the largest year over year gain since 1987 when Case-Shiller was created. Prices are up 43.7% since the 2006 peak. Phoenix remains the city with the largest year over year appreciation at 32.4% in July.

Final Thoughts:

While we still face obstacles, uphill battles, and constant change; remember residential real estate just pulled us out of the shortest recession in history. The strength of the real estate market is what gave it the ability to save the economy. That strength was created by real demand, not loose credit, and seemingly limitless speculation.

Copyright 2021 Sarah Perkins

Sarah Perkins is an award winning account executive and has been in title sales since 2004. As the Director of Industry Research & Senior Account Executive, Sarah’s role is to bring real estate transactions to Navi Title. Sarah supports her clients by helping them navigate the ever-changing real estate space through thorough research and understanding of current trends impacting today’s home buyers and sellers.

Leave a Reply