Maybe the 10 years of growth were the calm before the storm. Even if it was not, the storm is here now. As we adapt to extreme inventory shortages, get comfortable in our masks, and try to stay healthy we now face a new challenge, surviving economic re-closures. Pending sales are up, buyer demand is up, inventory is down.

“This has been a spectacular recovery for contract signings, and goes to show the resiliency of American consumers and their evergreen desire for homeownership,” NAR Chief Economist Lawrence Yun said, “This bounce back also speaks to how the housing sector could lead the way for a broader economic recovery.” I hope that real estate can continue to lead the economy towards recovery despite the significant headwinds we are now facing.”

The AZ Market:

Cromford Market Index (CMI): The CMI is the best leading indicator available (balance is 100, above 100 is a seller’s market and below 100 is a buyer’s market. Prices rise at 110 and drop at 90). Yesterday it was 258.3, higher than the pre-COVID peak of 241 and significantly up from the bottom of 145.2 we hit on May 15. Up over nearly 26 points since July 1.

Supply: Our local inventory has been dropping every day since May 12. As of yesterday, our inventory is 58% below normal. Our total active inventory is down nearly 28% year over year. That sounds like a lot; then when we remove under contract accepting backups (UCB) we are down 42% year over year. We desperately need more listings.

Demand: Pending sales are up over 6% month over month and up 17% year over year, which is a big deal given how much lower our inventory is. Our demand is 7.7% above normal and increased by nearly 6% in the past fourteen days. According to Showing Time, in AZ, physical requests which recovered and from the March-April drop are dipping again, likely due to the low inventory. We are now 9.6% down year over year and 17.8% off the pre-COVID peak. Again, buyers cannot look at (or buy) houses that are not for sale.

Sales & Prices: Phoenix’s closed sales are up 5.5% year over year. The median sales price is up 8.2% year over year.

Southeast Valley New Listings, Pendings, and Closings: This week over week comparison for Tempe, Mesa, Chandler, Gilbert, Apache Junction, and Queen Creek since March 15 shows this week’s increased demand and decreased supply. Closings always increase at the end of the month.

Other AZ News:

- Amazon paid $19.85M for 91.5 acres in Goodyear.

- Mountainside Fitness is suing Governor Ducey over the recent executive order closing gyms due to the surge in new COVID cases in AZ. The gym alleges that the order violates the AZ constitution by not allowing the company to prove that they are not a health risk.

- A partnership with Davcon Aviation and Mesa Hangar to create a $60M aviation project breaks ground in a Mesa opportunity zone.

- Wallethub released a study of the 2020 best and worst cities for first time home buyers. Gilbert ranked #5 and Chandler ranked #11. For the full list of cities and their rankings: https://wallethub.com/edu/best-and-worst-cities-for-first-time-home-buyers/5564/

Unemployment:

Initial unemployment claims this week dropped again to 1.3 million, slightly lower than the previous week’s 1.5 million, which continues the weekly decline every week since the end of March.

4.8 million jobs were added in June dropping the unemployment rate to 11.1% from May’s 13.3%. According to the US Department of Labor, the real estate sector, not including rentals, added over 18,000 jobs. The late June re-closures and re-opening delays will be seen in July’s unemployment report. Most economists are not as optimistic as they were mid-June. While jobs are still down 14.7 million since February, the 7.5 million total jobs regained in May and June is quite impressive.

66.5% of the unemployed are under 35. And of that group, 53.1% are under 25. According to the NAR buyer and seller report only 3% of homeowners are under 25.

Forbearance:

Of all active mortgages in forbearance that are past due on their payment, 77% have at least 20% equity in their home. At least 90% have positive equity, reducing the likelihood of a flood of foreclosures.

Mortgages in forbearance dropped for the third week in a row. According to the Mortgage Bankers Association, 8.39% of mortgages are in forbearance, down from 8.47% last week. Borrowers are opting out and looking at other relief options.

Emerging Trends:

- Historic low rates have made homes more affordable despite the higher price tags. According to NAR today only 14.6% of income is needed to make a mortgage payment. In June of 2018 it was 18.2% and the historic normal is 21.2% of income.

- After a decade of growth in public transportation use, the car is king again. More people are leaving city centers where cars are less necessary and going to smaller metros with fewer public transportation options.

- After decades of closures, drive-in movie theaters are making a come back. Pop-up drive-in theaters are emerging in mall parking lots and other unused large open commercial spaces.

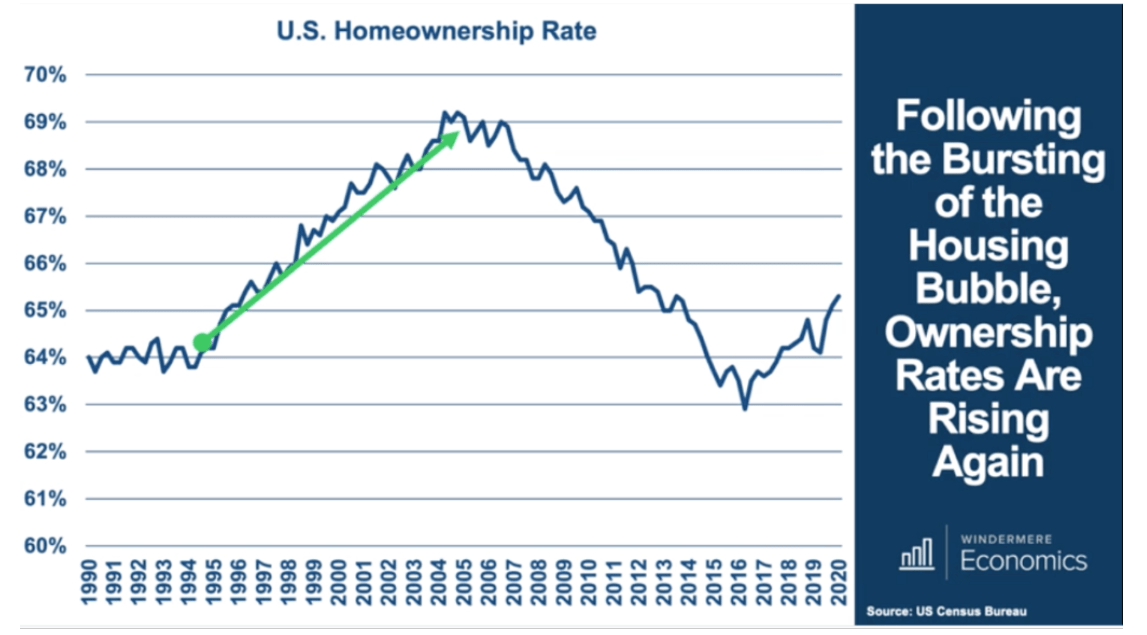

- Homeownership rates increased from 1990 to 2006. In 2006 they began dropping bottoming out in 2016 at levels lower than they have been since 1990. Since 2016 they have again been on the rise. However, builders have not kept up with the rising homeownership rates leading to historically low inventory levels today. These low inventory levels are pushing prices up faster than incomes are rising.

- In response to the skyrocketing home prices, state and local legislators across the country working to pass upzoning laws. This would allow multi-family housing structures on land zoned for single-family residences. Oregon and Minneapolis passed these laws in 2019. These laws face staunch opposition as multi-family buildings often reduce the value of the neighboring single-family properties.

- Commercial mortgage-backed security delinquency rates increased to 10.32% in June, nearly hitting an all-time high. The June 2019 delinquency rate was 2.84%.

- According to the Federal Reserve, the results for the Dodd-Frank mandated stress tests required for banks show that the largest American banks (Wells Fargo, Citibank, Chase, and Bank of America) could lose as much as $47.6 billion on commercial real estate loans over the next two years.

- According to a study by Apartment List released Wednesday, 32% of Americans did not make a complete July housing payment. Of the 32%, 13% made a partial payment and 19% made no payment. 36% of renters did not make their full payment. Of the 30% of homeowners that did not make a full payment, 18% made no payment. These numbers seem very high.

- *Please note this info from June data, “It continues to be the case that the majority of payments missed in the first week of the month are made up with late payments. 89 percent of respondents reported that they had paid their June bill in full as of the first week of July. This is consistent with the end-of-month payment rate for prior months.” For more details https://www.apartmentlist.com/research/july-housing-payments

Other Real Estate News:

- Last week the US Supreme Court ruled that the Consumer Financial Protection Bureau (CFPB)’s structure is unconstitutional. The agency was created in the Dodd-Frank Act of 2010 to protect consumers from predatory lending practices. They ruled that the whole agency is not unconstitutional. Chief Justice John Roberts stated, “The CFPB’s single-director configuration is also incompatible with the structure of the Constitution, which — with the sole exception of the Presidency — scrupulously avoids concentrating power in the hands of any single individual.”

- Last week Airbnb announced new policies to crack down on party houses to further prevent large gatherings, especially as COVID cases surge across the country. Renters under 25 who have fewer than 3 positive reviews will not be able to book single-family residences near where they live.

- The new Chinese National Security Law cracking down on dissent in Hong Kong is making American real estate investors question their investments. Soon Hong Kong may no longer be a destination for future real estate investment. These investors are looking at other global opportunities.

- Quicken Loans filed for IPO as Rocket Companies.

- The real estate industry received 3% of the total money distributed by the Paycheck Protection Program (PPP)

- Economist Elliot Eisenberg said, “As part of the CARES Act, lenders that allow borrowers to defer debt payments may not report those payments as late to credit-reporting firms. As such, borrower FICO scores are no longer as good at separating good borrowers from the bad. As a consequence, many lenders are compensating by tightening standards for all consumer loans, credit cards, and auto loans, depriving deserving households of credit, until they can figure out Plan B.”

Final Thoughts:

NAR expects to see a total of 4.93 million resale transactions in 2020. In 2021 they project resale transactions to hit 5.35 million. In 2019 we had 5.34 million resale transactions. Some experts say these are lofty goals. However, with proper guidance and education, we can make it happen.

This is a great time to sell. Do not get distracted by the negative media; the best way to be part of the solution is by getting accurate information out and guiding your clients with the facts.

Copyright 2020 by Sarah Perkins

Sarah Perkins is an award winning account executive and has been in title sales since 2004. As the Director of Industry Research & Senior Account Executive, Sarah’s role is to bring real estate transactions to Navi Title. Sarah supports her clients by helping them navigate the ever-changing real estate space through thorough research and understanding of current trends impacting today’s home buyers and sellers.

Leave a Reply