Despite our fear of change, humans are quite resilient and are far more flexible than we realize. Quite often, change is good. Demand is declining and seasonality is beginning to emerge in the market. I am hearing stories about an FHA buyer who finally had a contract accepted and a seller who agreed to a few concessions. This is good news for our exhausted buyers; they need some wins too. This is how the machine is supposed to work.

Demographics:

The post-2008 market crash recovery was the weakest recovery in real estate history. Nationally we have been in a seller’s market since 2012, here in AZ it has been since 2014 (we had a deeper hole to climb out of than most of the country). From 2017-2020 resale closings ranged from 5,340,000 (2018) to 5,640,000 (2020); that is not a huge variation.

There are more than 32,400,000 Americans aged 27-33. This is the largest group, in the largest generation and this is the prime time for getting married, having babies, and buying houses. Logan Mohtashami, senior economist at HousingWire says, “This is when people date, mate, and buy real estate.”

The demand wasn’t here 10 years ago but it is here now and likely to stay elevated through the end of 2024. The combination of high demand and low inventory indicates we will stay in a strong seller’s market for years to come. The biggest problem buyers face today is declining affordability.

New Construction:

Builders have been underbuilding since 2009 due to the extremely slow recovery. The baselines for months of inventory for new homes is different from resale. At 6.5 months, builders stop building. At 4.4-6.4 months builders are ok as long as sales are consistent. Under 4.3 months builders are happy and building as fast as possible. Nationwide there is a 3.3 month supply of new homes. The building frenzy is warranted.

While many are looking to builders to solve our inventory crisis and therefore aid in slowing this massive appreciation, builders will not overbuild. Builders are sellers, they want to maximize profits too. Like many of us, they too remember the pain of the crash and adjusted their business models accordingly.

Lumber costs are the most notable, having nearly tripled in the past 12 months, but other material costs have increased also. Combine that with the labor shortages and huge demand, costs continue to rise for builders, who then push the additional costs to the buyers.

Institutional Investors:

Since the end of the Great Recession, institutional investors have purchased over 7M single-family homes to keep as rentals. These buyers are home rental firms, like Invitation Homes which owns about 80,000 houses in 16 markets, private equity, pension funds, sovereign wealth funds, etc.

According to John Burns Real Estate Consulting, institutional investors are currently purchasing about 20% of all single-family homes in the US. Due to the continuously climbing rental rates in Phoenix, these buyers are purchasing about 30% of the single family supply. They pay cash and will go over the asking price in order to secure the property; something many buyers simply can’t compete with. Additionally, these properties are held longer than a typical owner stays, meaning these properties are being completely removed from the market.

National Real Estate:

Many industry experts predict that 2021 will have more sales than 2020 despite the low inventory. NAR predicts 6.5M resale closings, which is significantly up from 2020’s 5.64M resale closings. We do have strong demand and the market is, very slowly inching towards thinking about maybe trying to get closer to being normal, demand is not booming, which makes me doubt that 6.5M sales projection.

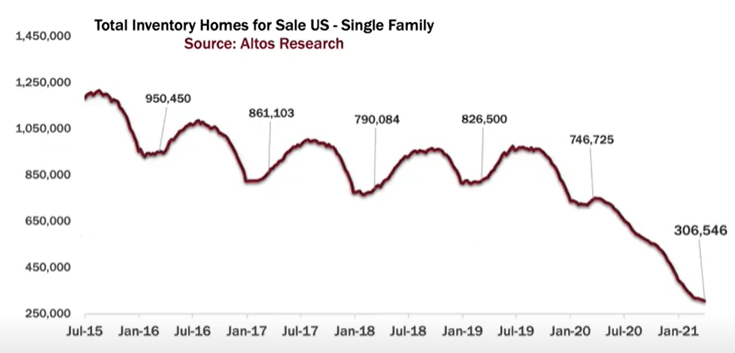

Single-family active listings declined by another 3,000 listings this week so we are now down to 306,546. We may have another week or two of declines and by May, it is likely we will start to see an increase in inventory. Inventory levels are expected to stay low for years but not at these low historically low levels.

Prices have stabilized, for the past 3 weeks, the median new listing asking price has remained at $350,000. Expect this to fall as we get later into the year. During normal cycles, more expensive homes are listed in the first half of the year.

While prices and inventory have started to stabilize, the speed of homes going under contract has not. 38% of single-family homes went under contract within hours of listing and 70% sold in less than a week on the market.

The AZ Market:

The Case-Shiller Index measures residential values using a very specific set of data and guidelines and runs a couple of months behind the current market. Many large institutions, including the US Census, use it to gauge appreciation. The most recent data is from January and it shows, for 20 months straight, that Greater Phoenix has the highest appreciation rate in the country. January came in at 15.8%. More info on Case-Shiller click here and here.

Demand is dropping, as of yesterday, it is 9.2% above normal. And inventory is increasing, it now only 77.7% below normal. Active listing supply is down over 70% from last year (during lockdown protocols). The median sales price is up over 18% year over year to $360,000.

Remember in January 2020, when Tina Tamboer with the Cromford Report told us to expect a 10% appreciation in 2020 and it was shocking? I do. A lot has changed since then.

Lending:

- Many experts believe that despite rising interest rates (with the exception of the past 2 weeks) buyer demand will not dampen. In a press release from March, Fannie Mae stated that while some buyers are being pushed out of the market, an ample amount of buyers remain.

- For the second week in a row, 30 year fixed mortgage rates declined. Despite the drop Freddie Mac expects rates to rise slowly throughout 2021.

- While interest rate increases often make people nervous, remember the largest home purchase year in history was 2005 and rates were about 7.5%.

- In March, for the first time in 15 months, purchase loan originations made up more than 50% of all originations.

- In March new home purchase applications increased by 12% from February.

- Purchase mortgage applications declined by 1% last week from the prior week. Refinances decreased by 5%.

Forbearance:

The forbearance numbers saw one of their largest improvements this past week, dropping down to about 2.3 million borrowers or 4.66% of loans. That is down from 4.9% the previous week.

“Almost 32 percent of borrowers in forbearance extensions have now exceeded the 12-month mark. In terms of performance, more than 88 percent of homeowners who have exited into deferral plans, modifications or repayment plans were current on their loans at the end of March, compared to 92 percent of all homeowners. The accelerating economic recovery in March helped more homeowners recover and become current on their mortgages, in addition to helping other homeowners with more stable financial situations exit forbearance.”

Mike Fratantoni , MBA senior vice president and chief economist

Policy:

President Biden’s first-time homebuyer tax credit has evolved and was submitted to Congress on Wednesday. In the current iteration of the legislation, it is less of a tax credit and more of a down payment assistance program offering up to $25,000. Eligibility requirements include but are not limited to buyers who have not owned a house in the past 3 years, none of the borrowers’ parents may have owned a house unless they lost it due to foreclosure or short sale, income limits, and additional funds are available to groups recognized as socially disadvantaged. For more information click here.

Real Estate News:

- SoftBank’s Vision Fund is investing $500M in digital mortgage start-up Better.com. SoftBank’s other investments include Opendoor, Compass, SoFi, and Doordash.

- Opendoor is expanding its buy box to include more expensive and older homes. Opendoor is also rolling out its own version of a preliminary instant offer shifting from a 24 hour response time to three minutes. This is to compete with Zillow’s Zestimate instant offer.

- After multiple failed attempts to acquire CoreLogic, CoStar, which is heavily involved in commercial real estate, plans to acquire Homes.com for $156M as it continues to enter the residential space.

- California Regional MLS, the country’s largest MLS with 104,000 members, has declared Saturday a business day. Some suspect it is to prevent a loophole in the Clear Cooperation Policy.

- The SEC is warning investors about an increase in “lawsuits alleging inadequate disclosure by SPACs.” Going public via SPAC has been perceived as a cheaper, easier process than via IPO. However, in November, Harvard published a study showing that SPACs are more expensive than an IPO and investors are paying those added costs, for now.

Final Thoughts:

Today’s market is nothing like that of 2005 but the intensity of it feels very similar. As the market begins to cool, fear will rise, the 2008 crash wasn’t THAT long ago, right? A lot has happened in 13 years.

That hasn’t stopped the housing fear Googling though. Searches asking, “When is the housing market going to crash?” increased by 2,450% in the past 30 days. Searches asking, “Why is the market so hot?” doubled in the past week. And searches asking “How much over asking price should I offer on a home 2021?” increased by 350% in the past week.

Let’s spread the word, housing is, hopefully, starting to normalize which is good for everyone. Prices will continue to rise but at a slower rate.

Copyright 2021 Sarah Perkins

Sarah Perkins is an award winning account executive and has been in title sales since 2004. As the Director of Industry Research & Senior Account Executive, Sarah’s role is to bring real estate transactions to Navi Title. Sarah supports her clients by helping them navigate the ever-changing real estate space through thorough research and understanding of current trends impacting today’s home buyers and sellers.

2 thoughts on “Greater Phoenix Real Estate Update 4/16/2021”