Consumer sentiment has the greatest impact on our economy. It is more powerful than any piece of information or event. With today’s incredibly polarized media where everyone has an agenda, it is almost impossible to get accurate information. The headlines often conflict with what is actually happening, let’s talk about the real numbers.

For example, look at the second quarter stock market returns versus the economic data. Investors have no idea why the markets ended so well when there was so much bad news in every headline. The S&P 500 increased by nearly 20%, the Dow Jones increased by nearly 18%, and the NASDAQ was up nearly 31%! Almost all of March’s losses were made up and the NASDAQ actually increased from previous highs. (Jeremy Kisner, Surevest Wealth Management)

Suze Orman, a personal finance expert, not a real estate expert, is advising that now is a bad time to buy a house. That is as helpful as a dentist doing your taxes. Unfortunately for us, she has a large audience.

Lendingtree released a study stating that 87% of home sellers are concerned about selling due to the pandemic, yet 372,000 homes sold in June. Our pendings are higher than they were 12 months ago and prices are increasing. Houses are selling faster today than they have in years.

Last week I wrote about a report, from Apartment List, stating 32% of Americans did not make their housing payment the first 3 days of July. The same report said 30% did not make their June payment in the first 3 days of the month. These numbers were so high I dug deeper and found better data.

According to the US Census Bureau Household Pulse Study, of the nearly 74 million renter-occupied housing units in the country, roughly 16% did not make their June payment. And of the nearly 150 million owner-occupied properties in the country, 5.5% did not make their June payment.

In Arizona, of the just over 1.6 million renter-occupied properties 9% did not make their June payment. And of the nearly 3.5 million owner-occupied properties in AZ, only 3.3% did not make their June payment. (US Census Bureau Household Pulse Study)

Forbearance:

Mortgages in forbearance declined again, for the fourth week in a row. 8.18% of all mortgages are in forbearance, down from 8.39% the previous week. (Mortgage Bankers Association)

One third of mortgages in forbearance are late on their payments. Two thirds are current. (KCM)

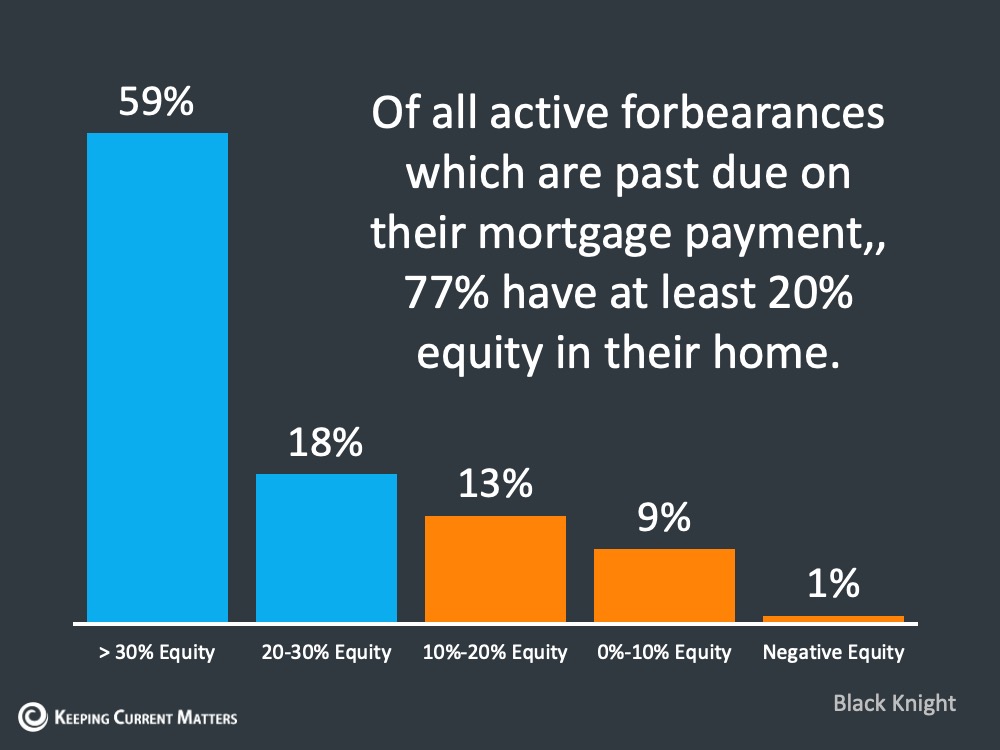

Going deeper, of all the mortgages in active forbearance that are late on their mortgage, 77% have at least 20% equity. Only 10% of the past due mortgages have 10% or less equity. (Black Knight)

Price Projections:

There is a wide range of price projections emerging from top real estate experts. Mortgage Bankers Association projects a 4% annual appreciation and Corelogic, a clear outlier, expects a 6.6% depreciation. David Childers at KCM reached out to the chief economist at CoreLogic asking about this projection and was told it was entirely based on expected low demand solely due to unemployment. They did not address the lack of supply. That seems very odd when supply and demand are the fundamentals of pricing.

Unemployment:

According to the US Census Bureau, 46% of the people who do not have a job and are over the age of 18 live in households with an income of less than $50,000 a year. These households tend to rent.

1.3 million people filed for unemployment for the first time this week, continuing the week over week decline for 15 weeks straight.

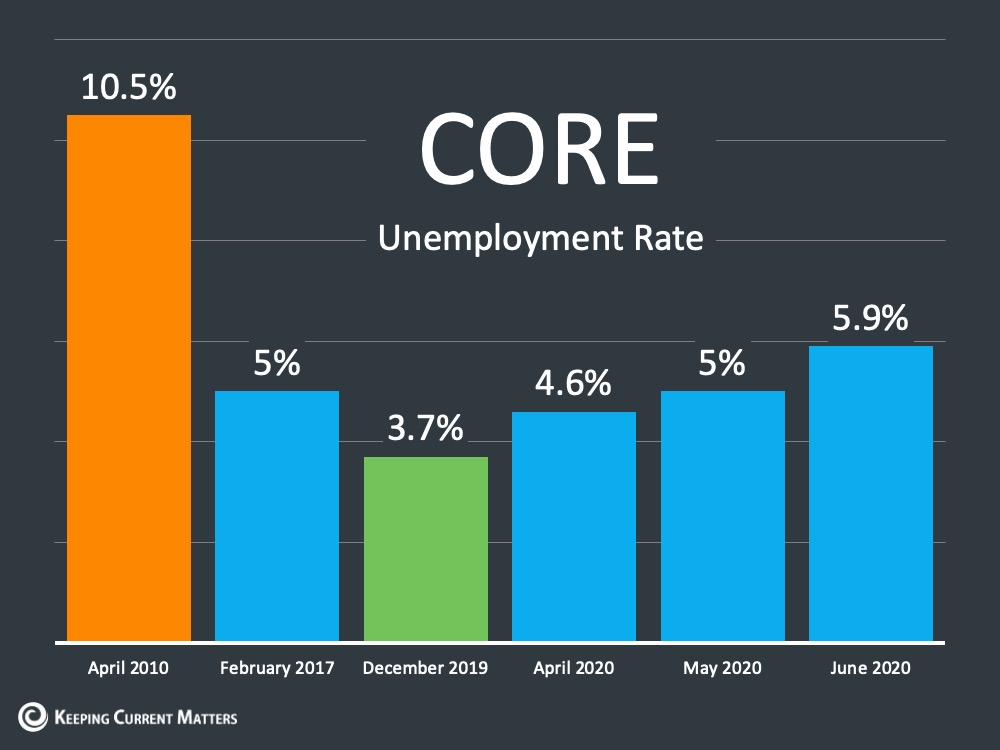

There are two types of unemployment temporary and Core or permanent unemployment. June’s Core unemployment was 5.9%. For comparison, it was 10.5% in April 2010 and 5% in February 2017. (KCM)

Future of Housing:

Windermere Chief Economist Matthew Gardner said, “We are exactly 120 days into this pandemic and, as much as there were some who fully anticipated that the U.S. housing market would have collapsed already, it simply hasn’t happened — and won’t happen.”

As economies reopen, we will likely see increases in listings. However, with the surges of new COVID-19 cases across the country (AZ isn’t the worst anymore!) sellers may delay selling, keeping inventories low and prices rising quickly.

As the CARES Act is set to expire at the end of the month, delinquencies may rise and that may impact housing however, with the high equity rates, the potential “distressed“ listings will still be regular sales.

The AZ Market:

Cromford Market Index (CMI): The CMI is the best leading indicator available (balance is 100, above 100 is a seller’s market, below 100 is a buyer’s market, prices rise at 110, and drop at 90). Yesterday it was 279.4, higher than the pre-COVID peak of 241 and significantly up from the bottom of 145.2 we hit on May 15. Up over 21 points in the past 7 days.

Supply: Our local inventory has been dropping every day since May 12. As of yesterday, our inventory is over 60% below normal. Our total active inventory is down 30% year over year. When we remove under contract accepting backups (UCB) we are down 43% year over year. We desperately need more listings.

Demand: Pending sales are up 16% year over year, which is a big deal given how much lower our inventory is. Our demand is 11.5% above normal and increased nearly 4% in the past seven days.

Sales & Prices: Phoenix metro area closed sales are up 10% year over year. The median sales price is up 5% month over month and over 11% year over year. Healthy appreciation is 3% annually.

Southeast Valley New Listings, Pendings, and Closings: This week over week comparison for Tempe, Mesa, Chandler, Gilbert, Apache Junction, and Queen Creek since March 15 shows the continuation of demand outpacing supply. Closings always spike at the end of the month.

Other AZ News:

- Phoenix ranks #16 in the country for in most valuable residential real estate with a total value of $484 billion. (Lendingtree)

- According to WalletHub Phoenix is the 41st most stressed-out city in the country. We have among the lowest financial, family, health, and safety stress but we are experiencing incredibly high work stress because we have the strongest job market in the country and have lost the fewest jobs. This means more of us are trying to juggle the stress of the world today while continuing to perform at work.

- Phoenix area builder permits pulled in June increased by 9.6% year over year. (Home Builders Association of Central Arizona)

- According to the Realtor.com Housing Market Recovery Index, the Phoenix metro area has completely recovered from the pandemic slow down. This index combines supply, demand, price, and days on market.

Emerging Trends:

- Realtor.com traffic hit an all-time high in June with 86 million unique visitors, breaking the previous record of 85 million in May. (Move.com)

- Household savings rates are up 8% year over year, the highest since the early 1990s. (KCM)

- Spending by the bottom 25% of earners has recovered from the 23% drop in March, while spending by the top 25% of earners is still down 17% though up from the 31% drop in March. The discretionary spending reduction continues to hurt the low-income earners who are the often the workers at salons, movie theaters, and restaurants. (Elliot Eisenberg)

- Commercial real estate investors are starting to buy office buildings at 10-30% discounts in gateway cities. (Bisnow)

- Meanwhile, industrial real estate sales prices continue to increase. (Bisnow)

Other Real Estate News:

- Mortgage interest rates hit all-time lows, again, keeping the demand high as every percentage drop equals roughly $40,000 of buying power.

- According to Zillow, luxury home listings are recovering quickly while affordable home listings continue to decline, down 29% year over year.

- Dotloop, the Zillow owned competitor of Skyslope, has a new third party data sharing policy. Agents using the platform need to opt-out of sharing the data rather than the typical opt-in. (Zillow)

- In October, when the US Supreme Court reconvenes, they will determine whether or not the structure of the Federal Housing Finance Agency (FHFA) is constitutional. They recently ruled that the structure of the CFPB was unconstitutional.

- According to the recently released Consumer Federation of America study, agent profiles on Zillow are the most useful for consumers; compared to Realtor.com, Yelp, Facebook, and Homelight.

- New Silicon Valley start-up, Juno, is “reimaging” multi-family building. The prop-tech company is looking to disrupt the building process. (Jim Dalrymple, Inman)

- In Fort Worth TX, a struggling multifamily property owner is suing the US Government challenging the eviction moratorium in the CARES Act. (Bisnow)

- Knock.com is pivoting their model and instead of purchasing property they now offer mortgage financing, bridge loans, and concierge services. They are no longer working direct to consumer and will only partner with real estate agents.

Final Thoughts:

The negative news is growing at an alarming rate and the headlines are misleading. With so much bad info, it is important that you talk to your clients about what is really happening in real estate. Share this info, make videos, call your sphere, continue being the solution during these uncertain times.

Happy Birthday Mom! I can’t wait until I can see you in real life again!

Copyright 2020 by Sarah Perkins

Sarah Perkins is an award winning account executive and has been in title sales since 2004. As the Director of Industry Research & Senior Account Executive, Sarah’s role is to bring real estate transactions to Navi Title. Sarah supports her clients by helping them navigate the ever-changing real estate space through thorough research and understanding of current trends impacting today’s home buyers and sellers.

This is very interesting, You’re a very skilled blogger. I have joined your rss feed and look forward to seeking more of your excellent post. Also, I have shared your site in my social networks!