Once again, today is all about the AZ market. On Wednesday, Lawyers Title hosted a presentation with Tina Tamboer with the Cromford Report. She always shares pertinent and timely information. Below I have combined a lot of her information from her presentation, along with additional information from my research.

Inflation:

According to Reuters, consumer price inflation increased by 0.8% from March to April, the largest increase since June 2009. It increased by 4.2% year over year, the highest since September of 2008. Experts blame supply chain challenges and last spring’s weak readings. Many economists believe has taken the brunt of inflation already. Consumers call it appreciation and economists call it inflation.

Why Do We Have a Housing Shortage?

From 2000 to 2009 we over-built for the population. From 2010-2020 we under-built for the population. In 2004-2006, speculation building on credit caused huge problems. When the lending dried up, we had huge price declines. This is not a gap that can be closed easily.

New Construction:

Material prices are going up. Lumber has increased the most at roughly 430% year over year. Eye On Housing is a great blog with lots of information. The increased cost of materials for the average new home is nearly $36,000. Condos are up $1,300. Apartments are up $119 a month. Builders pass the costs to the consumers. Builders are begging appraisers to take into consideration the increased material when appraising. If an appraisal doesn’t come in at contract then the builders will struggle to sell.

Personal income growth soared in 2020. People did not take fancy vacations, spent less on gas, spent less on eating out, etc. This helps offset the rise in prices.

Single-family permits through March are up 26.7%, year over year. We are at elevated levels. People are afraid of all the building. We haven’t seen this many permits since 2006. The builders may not build all the houses they have permits for.

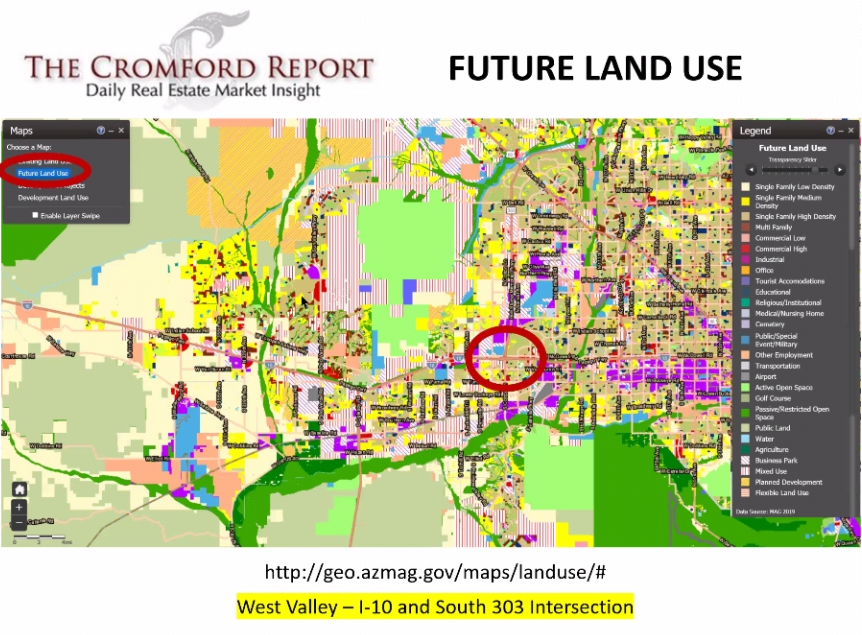

To see the existing and future planned developments visit http://geo.azmag.gov/maps/landuse/

Blue is vacant land, which there is a lot of in the northwest valley by the I-17 and 303. The future land use shows upcoming development. A lot is going in around the Taiwan Semiconductor Manufacturing Company.

Yellow is SFR. High density is tan. Pale yellow is low density, yellow is medium density. Affordable housing to come in the NW valley also. Green is agricultural land, light green is passive land use. Tons of SFR building on the west side. Lots of industrial, which brings lots of jobs.

Many people are worried about water. The future plans show development in place of agriculture. Agriculture uses far more water than developments do.

DR Horton is buying large quantities of land as far south as Eloy and that huge Superstition Vistas area just south of Apache Junction.

Employment:

US unemployment rate: 6.1%

AZ unemployment rate: 6.7%

The labor force increased. Our base has recovered for people who are already working. The numbers don’t look great but we are improving. A lot of service sector jobs are coming back and restaurants and hotels are hiring.

- Month over month, Arizona nonfarm employment increased by 16,000 jobs.

- Nine of the eleven major sectors gained jobs.

- Year over year, Arizona nonfarm employment declined by 2.9%, while US nonfarm employment declined by 4.4% YoY.

- Year over year, ten major sectors lost jobs; one major sector gained jobs.

- The Arizona unemployment rate decreased to 6.7% in March 2021 from 6.9% in February 2021.

- Month over month, the Arizona labor force increased by 6,749 individuals

- As of March 2021, the Arizona labor force is larger than it was prior to the COVID-19 pandemic.

Population:

US population grew by 0.4% we grew by 1.8%. Losing population slows housing growth because fewer people are in houses and buying houses. Our growth came from domestic migration with the largest populations coming from CA, IL, WA.

Forbearance:

When forbearance ends it will not rain houses. There are about 2.2 million mortgages or about 4.2% in an active forbearance plan. There have been huge improvements in forbearance counts. 54% have successfully exited the plan. If all states are equal, each would have about 46,000 properties in forbearance.

Lots of people are exiting and are current, about 47% are ok. The struggling amount is about 16.4% and that leaves us 7,128 new listings for all of them if they are all struggling and need to sell right away. That is not enough to cause a problem.

Greater Phoenix economic council has diversified employment over the past 10 years. NV, TX, LA, FL, NJ are going to have more issues with forbearance exits because of the business. We will probably not even have as many as 7,000.

For more information on forbearance, check out my latest AZ Forbearance Update, here. Properties that are late and in forbearance are still counted in the delinquency numbers. For more info on delinquencies, check out my AZ Forbearance Update from the end of April, here.

Inflation:

Overall including gas is 2.6%. (April came out Wednesday) People are stressed, gas has seen an impact. The overall long-term inflation rate is 3%. We are within range. We were at 2.9% right before the pandemic. We have been under 2% and have gotten spoiled. We like low inflation. Low inflation usually follows not-so-great times in our lives. There is no real correlation between inflation and appreciation. When we are in a balanced market appreciation matches the rate of inflation, when it is low, things are not good. Probably won’t have an impact on housing.

Luxury Market:

The luxury market and Bitcoin have spiked in 2021. Luxury increased in 2020, but this year it is crazy. It is not just from the CA buyers. The $2 million market is booming! Only Bitcoin and luxury real estate have exploded to this extent. No supporting data, only circumstantial.

Recording only tells us whether or not they have a loan. Not how they paid for it, with USD or crypto

Bitcoin is the only thing that has gone up as fast as real estate, if it drops off, will we see a drop off?

Bitcoin in real estate has been a big headliner for a year. People are buying with crypto. Who are we attracting to Phoenix? A lot of tech companies from CA. Again based on circumstantial info.

Cromford Market Index:

Available on the main page of the Cromford Report: https://cromfordreport.com/ (without a subscription)

- 100 is balanced and prices rise at the rate of inflation, below 100 is a buyer’s market, above 100 is a seller’s market, prices drop below 90, prices rise at 110.

- On 2/5/2020 we were at 215.1

- On 3/20/2020 we were at 241

- On 5/15/2020 we were at 145.2

- Yesterday we were at 461.2

- We peaked on 3/14/2021 at 514.9

- Prior to this run, the previous peak was 312.9 in the spring of 2005.

- CMI is the predictor, it moves first and then appreciation follows. Cannot predict the CMI.

The CMI is declining. This is where we see the shift taking shape. Demand is not falling as fast as it was earlier in the year. Since December demand has been dropping but inventory was dropping faster, keeping the CMI high. When the CMI started declining it was at a rate of about 8 points a month, then 5 points and now we are at 2.3 points a month. Demand has stopped dropping and actually increased yesterday, supply has actually risen which is great news. When demand goes below normal is when we see fewer transactions. Homes are still appreciating. It is good to see demand level off. Under 90 is low demand.

There are still multiple offers and many sales over asking. Measure the temperature 514.9 degrees to 461.2 degrees; the market is still super-hot.

How long will it take us to get to balance? It took 8 months to drop in 2005. If we stay at this rate, we are looking at 11.5 months to get to balance, which is May of 2022. It is measuring like 2005 which only means that prices are going up at a slower rate.

Appreciation rates respond to markets. Appreciation rates will continue rising for the next 3-6 months. Annual appreciation rates rise when CMI drops. Price is a lagging indicator. It shows us where we were. CMI is a leading indicator, it tells us will happen.

Yes, it is still a good time to buy because you always want to buy in a seller’s market, it is a winner’s market. Watch the equity grow. If it drops, it is ok because you have a down payment. Buyer’s markets are losers markets, everyone loses in a buyer’s market, and prices keep dropping during a buyer’s market.

Just because it goes up does not mean that it will go down. The worst case is going down to balance. Nothing is indicating a decline in prices and no one is predicting one. If supply and demand come together and demand is below balance, the market will be slow and boring with fewer transactions. If supply and demand come together with demand above balance, then the market will be fast-moving, exciting, and have lots of transactions.

There are 5 cities with increasing CMIs: Fountain Hills, Glendale, Goodyear, Paradise Valley, and Surprise. The factor for downward trend is affordability and pent up demand that created a surge, and buyer fatigue.

Affordability:

Affordability in Q1 2021 did not drop below 60, which is the bottom of the unaffordable range. The median family income is $79,000 a year. The national affordability score is 63.1 and for Phoenix, it is 62.8.

Rentals are not affordable, mortgages are but not rents year over year. Affordability will be tough on rentals. With FHFA 7% portfolio limits for 2nd homes, any added expense will be pushed to the renter, further challenging renters.

Supply:

Inventory is rising. It doesn’t usually rise in May, going against the local seasonality trends. This is something to watch. People aren’t going to notice it yet. When you are supposed to be going down and are going up instead it shows a shift in the marketplace.

Demand:

- Restrained by lack of supply, not so much by demand.

- 57.1% of sales closed over asking in April.

- $16,100 median over asking amount.

- Larger homes are appreciating more and faster. This is not normal for us or really anywhere.

- The median sales price for single-family homes has reached $418,500, which is a 33% year over year appreciation rate.

Summary:

- The seller’s market is weakening. Sellers won’t notice but we do.

- Supply: 77% below normal but increasing.

- Demand: 7.6% above normal, leveling off.

- 57% of April sales closed over asking for a median amount of $16,000.

- The median days on market is 6 (hasn’t changed in 7 weeks)

Sarah Perkins is an award winning account executive and has been in title sales since 2004. As the Director of Industry Research & Senior Account Executive, Sarah’s role is to bring real estate transactions to Navi Title. Sarah supports her clients by helping them navigate the ever-changing real estate space through thorough research and understanding of current trends impacting today’s home buyers and sellers.

Leave a Reply