One year ago yesterday, the World Health Organization officially declared the coronavirus a worldwide pandemic. Despite our efforts, no one accurately predicted the following 366 days. The light at the end of the tunnel is getting brighter. Kids are going back to school, vaccines are being distributed, the economic conditions are improving, and residential real estate – the sector that carried the entire economy for a year.

Real Estate Disruption:

Two weeks ago I wrote about real estate becoming less grassroots, more Wall Street, and Zillow’s new Zestimate. You can read the update here. On Wednesday, Brad Inman wrote about 8 of the 10 largest real estate firms being publicly traded. Those firms represent nearly 45% of all Realtors. There are upsides and downsides to Wall Street in real estate. Read his article here.

Last year Compass lost $270 million (details below). Zillow’s iBuyer and Opendoor combined lost $607 million in 2020. In 2019 they lost a combined $650 million. How is it that two companies can lose over $1.2 billion dollars in two years and remain in business? These companies are spending big money fighting for market share in the strongest sector in the economy. Why? Because US residential real estate is valued at $39.3 trillion, which is nearly double the 2019 US GDP ($21.4 trillion) and it is the nation’s most valuable asset. It is followed by equities at $37.2 trillion and commercial real estate at $20.4 trillion. With so much value in residential real estate and it being an industry that dodged disruption for a long time, Wall Street and Silicon Valley will continue to create and fund disruptors until they can figure out how to turn a profit.

Compass:

Compass, one of the fastest-growing real estate firms in the country has made a lot of waves over the past few years spending big money on advertising and up to $250,000 agent signing bonuses. CEO, Robert Reffkin has raised millions from investors like Softbank, Opendoor’s biggest investor before going public. Compass is spending money buying tech companies and Realtors. They recently filed their IPO and showed that despite bringing in $3.7 billion in revenue in 2020, it had a net loss of over $270 million. The filing notes stated, “may not be able to achieve profitability and we may continue to incur significant losses in the future.” Reasons given are market expansion costs, declines in real estate sales, and increased competition in the market. Compass is counting on its tech investments to drive profits.

Opendoor:

On its recent earnings call, CEO Eric Wu said that Opendoor’s offer requests have increased 50% year over year. By the end of 2021, Opendoor will have doubled number of markets and will continue entering new markets, with a goal of being in 100 markets and serving 70% of US homes. In order to gain market share the company has expanded its buy box and is continuing to build its vertical integration by offering title, escrow, and mortgage services along with traditional brokerage services.

REX’s Lawsuit:

On Tuesday, discount brokerage, REX, filed an anti-trust lawsuit against Zillow, Trulia, and NAR. The company charges roughly 2% commission, 1% goes to the brokerage and 1% to the listing agent. It is not a member of any MLS and does not pay buyer’s agents a commission. REX markets all of its listings online, including on Zillow and Trulia. The complaint states that NAR’s rules, enforced by the MLSs, requires that a seller pay a buyer agent’s commission. Now that Zillow is also a licensed brokerage it has joined the MLSs and must follow local MLS rules. As Zillow has adjusted its platform to be compliant, non-agent listings are now in a different section from the agent-represented listings. Zillow’s spokesperson said Zillow’s goal is to change the MLS rules so that all available listings would be located in one place on the site, allowing for easier searching. However, currently, the MLS does not allow for that.

National Real Estate:

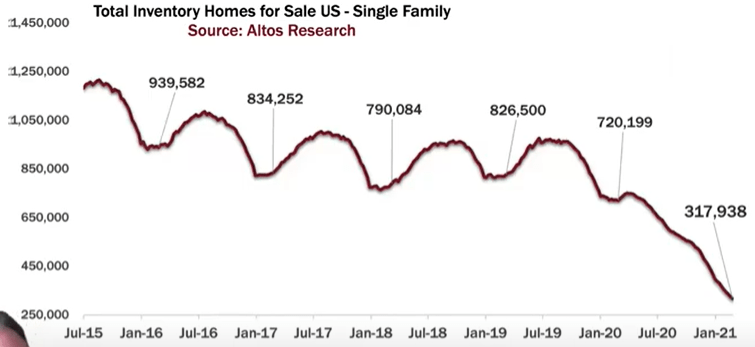

Nationwide there are just under 318,000 active single family listings, a 55% decrease year over year.

One of the reasons for our low inventory nationwide is due to the low interest rates we have had for over 10+ years. 5% in 2009 was a record low. While our housing market recovered slowly after the Great Recession, many people moved up but kept their previous homes as rentals. Since 2013 about 7 million single family residences have become rentals, removing their availability from the resale market.

The supply to demand imbalance continues to push up sales prices and more properties are selling for over asking than ever before. Nationwide we hit a record low for the amount of homes taking a price reduction, the average is about 35% of active listings have at least one price drop before going under contract. Today it is just under 17%.

The AZ Market:

Here in Phoenix 44% of sales in the past 30 days closed over asking.

Greater Phoenix has fewer than 3800 active listings and only 2700 active single family homes available which explains our 19.5% year over year appreciation.

Join us today for a Zoom meeting at 11am for a deep dive in the Greater Phoenix market with Tina Tamboer with the Cromford Report. To register, click here.

Lending:

Mortgage interest rates tend to follow the 10-year treasury yield so it is often used to predict mortgage rates. This chart shows them moving together for the past 50 years.

Going deeper, here they are for the past 10 years. The 10-year treasury rate has been increasing since October and interest rates only started catching up in February. An increasing treasury rate means a growing economy because as the treasury rate goes up, investors become more confident in the market.

Last week purchase mortgage applications were up 7% week over week and 2% year over year. Demand remains higher than supply, both nationally and locally. It is impressive that applications increased when rates have increased as quickly as they have. A big reason for the continued demand, according to several leading economists, is based on today’s demographics. The largest group of the largest generation is about 26-34; prime home-buying age. These ‘Replacement buyers’ as some call them, will keep demand high through the end of 2024.

For forbearance and foreclosure news, check out my update and video from Wednesday, here.

Real Estate News:

- UWM, the country’s largest wholesale lender recently announced it will not work with mortgage brokers who work with Rocket Mortgage or Fairway Mortgage. Does this set a precedent of big companies stating, “If you do business with them, I will not do business with you.”?

- Walmart is partnering with Ribbit Capital, a fintech investment firm to create a new fintech that will offer “innovative and affordable” financial products. They even hired the head of Goldman Sachs’ consumer unit to run it. This is in addition to Walmart’s debit, credit, and check cashing services. While they haven’t specifically said they are going into mortgages, many experts in the field believe that is exactly what Walmart is creating, affordable mortgages.

- Two weeks ago Federal judge in Texas ruled that the CDC’s eviction moratorium is unconstitutional. The court stated that Congress lacked the authority to give the CDC power to halt evictions, and that the moratorium infringes upon landlords’ rights under state law. The DOJ promptly filed a notice to appeal the ruling.

- Initially created for apartment complexes, SmartRent (based in Scottsdale), which offers home technology services just announced a $31 million partnership with home builder, Lennar. One of SmartRent’s features is self-guided tours which allows the perspective buyer to tour the property at any given time (scheduled a little as 1 minute ahead of time, online). The company’s website states this allows builders longer tour hours and reduces a builder’s Realtor costs.

- Another commercial property management company, Jones Lang LaSalle, is getting into the single family rental market.

Final Thoughts:

Logan Mohtashami of HousingWire said, “Once schools are open again, parents will be free to re-enter the job force: By September 2022 or earlier, we should have regained all the jobs lost to COVID-19. These positive economic factors warrant higher mortgage rates as we are no longer in recession in America. Now, we want to get all the jobs back that COVID-19 took from us.”

Please share this with your colleagues and clients.

Copyright 2021 by Sarah Perkins

Sarah Perkins is an award winning account executive and has been in title sales since 2004. As the Director of Industry Research & Senior Account Executive, Sarah’s role is to bring real estate transactions to Navi Title. Sarah supports her clients by helping them navigate the ever-changing real estate space through thorough research and understanding of current trends impacting today’s home buyers and sellers.

Leave a Reply