Real estate continues to normalize and shift from an extreme seller’s market to a less extreme seller’s market. Both the leading and lagging real estate indicators illustrate a slowly moderating housing market. The numbers show that things are changing, nothing is happening too quickly, so the movement is relatively healthy and going in the right direction. Buyers have more options and sellers are making some concessions.

Yet we face a lot of unknowns. Is this inflation truly transitory? Will the mid-September expiration of the expanded unemployment benefits drive employment growth? How many houses will actually be foreclosed on once the foreclosure moratorium is lifted on 7/31? And how long will that process take? How many renters will be evicted once the eviction ban is lifted on 7/31? What will the proposed infrastructure bill actually look like and how much will go to housing? When will the Fed taper its MBS purchasing? What about the rising COVID numbers?

Economy:

In a recent podcast, economist Dr. Peter Linneman discussed real estate and the economy with Willy Walker with Walker & Dunlop, a large commercial lender. These are some of his main points:

- Consumer inflation is transitory because inflation was negative last year. However, asset inflation has been significant for nearly a decade. (Greater Phoenix housing bottomed out in August of 2011 and homes have been appreciating since September of 2011.)

- Expect huge employment growth in September, and not before then, because the additional $300 a week in COVID unemployment benefits expires on 9/6/21.

- In 2020, about 300,000 Americans inherited $50,000 or more; 3 – 10 years earlier than expected due to COVID deaths. This created a large group of unplanned home buyers who otherwise would have waited years for the down payment funds.

- While he agrees with many other housing experts that we have been under producing for well over 10 years, he disagrees with NAR which states that nationwide we are short 6.8 million units, he thinks the deficit is closer to 3 – 4 million units. Ivy Zelman thinks it could even be closer to one million. He said in multi-family our deficit is about 700,000. All reasons for continued price increases as long as demand remains, but not a dire situation.

- Expect another era of roaring 20s. There is a lot of money in the system and not a lot of reason to pull it out, if greed turns to fear there will likely be a correction. Rates will stay low, the Fed will not raise them because they need to keep Federal debt cheap so the government can afford the debt. Additionally, he does not see the Fed tapering its monthly bond and MBS purchases. It has kept the market very liquid. The growth may slow but will stay positive.

- We need to expand to capacity. Supply is lagging. During the pandemic lockdowns, we continued to consume but did not replace what was consumed. This expansion will drive growth and the roaring 20s, though it will be bumpy. The growth will not last forever, do not fight it, asset ownership will create wealth, spend wisely.

National Real Estate:

- According to NAR, the median existing-home sales price is up 23.4% year over year and after four months of declines in sales, in June, existing home sales increased by 1.4% from May.

- The frenzy is calming and the sky rocketing, year over year appreciation rates are just starting to slow.

“At a broad level, home prices are in no danger of a decline due to tight inventory conditions, but I do expect prices to appreciate at a slower pace by the end of the year. Ideally, the costs for a home would rise roughly in line with income growth, which is likely to happen in 2022 as more listings and new construction become available.”

-Dr. Lawrence Yun, NAR Chief Economist

- Condo sales are booming. They increased by 22.8% in the first 12 weeks of 2021 with a year over year appreciation rate of 20%.

- In June, 65% of offers written by Redfin competed with multiple offers, down from the April peak of 74.1%.

- Single family active inventory is up 21% since the beginning of May.

“Supply has modestly improved in recent months due to more housing starts and existing homeowners listing their homes, all of which has resulted in an uptick in sales. Home sales continue to run at a pace above the rate seen before the pandemic.”

-Dr. Lawrence Yun, NAR Chief Economist

- Total inventory is up nationwide, giving buyers welcomed relief with slightly more options as inventory levels remain low.

The AZ Market:

- Both existing home and new construction home sales prices are up by nearly $100,000 year over year or 27% and 25% respectively.

- New home sales declined by 16% from June to July, yet strong demand remains.

- Single family rents increased by 6.6% in May, year over year. Phoenix once again saw the largest year over year price increase at 14% followed by Tucson (11.1%) and Las Vegas (10.7%).

- Apartment rents are up 5.8% over the past three months and 10% year over year.

- Arizona tourist spending declined by 41% in 2020 from 2019. In order to boost tourism, Governor Ducey recently announced the Visit Arizona Initiative which will utilize $101.1 million of federal relief funds.

- At 4700, Phoenix tops the DeedClaim’s list for having the largest housing shortage in the country while New York City has the largest surplus. Of the 149 cities researched 24 have housing shortages, these are the top 20.

New Construction:

Builder confidence, while still very high, declined by one point to 80 in July due to ongoing labor shortages and the high prices of materials.

New construction mortgage applications declined by 3% in June from May and was down 23.8% from last year. 2020 was the biggest new construction year since 2006.

In June, new single family starts are up 6.3% from May and up 29.1% year over year. Which is good news as completions were down in June by 6.3% from May.

“In other words, builders aren’t hedging long-term plans on short-term improvements after the past year of pandemic challenges. As factors like materials costs stabilize over the next three months, buyers may start to see some inventory and price relief in the new construction market.”

-George Ratiu, Realtor.com Senior Economist

Lending:

The adverse market fee, which was a 0.5% fee added to Fannie Mae and Freddie Mac refinances, has officially been axed. Starting August 1, the FHFA will no longer collect this fee. This is welcomed news for borrowers and the mortgage industry.

In June, second-home mortgage rate locks declined by 11% year over year. Much of the decline is attributed to Fannie Mae’s and Freddie Mac’s cap on second home and investment property mortgages at only 7% of total loan volume.

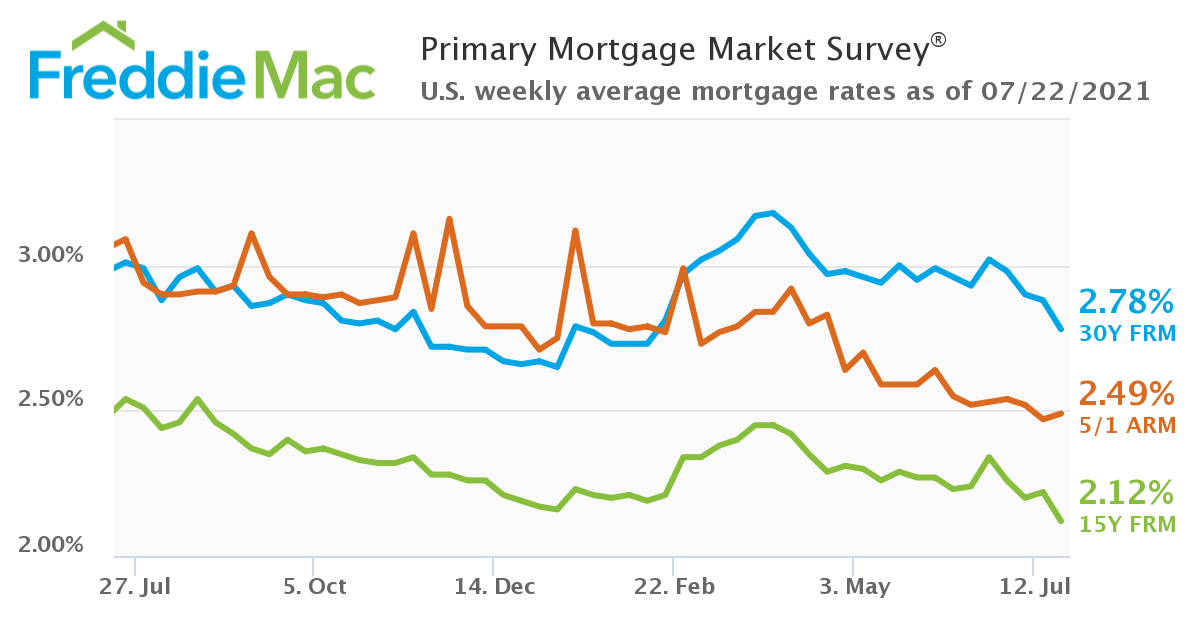

Mortgage rates dropped again, and the 15-year mortgage reached an all-time low.

Despite money being so cheap, cash purchases are on the rise. Through April of this year, 30% of purchases are with cash, up from last year’s 25.3%.

Real Estate News:

- In 2019, Blackstone, an investment management company with $649 billion in assets, attempted to exit residential real estate investments when it sold its interest in Invitation Homes. The exit did not last very long, in May Blackstone announced the roughly $1 billion purchase of 5,800 apartments in San Diego County with the promise to keep rents affordable for tenants earning 80% or less than the area’s median income. In June, Blackstone announced a $6 billion purchase of Home Partners of America which owns more than 17,000 single family rentals across the country. And this month Blackstone announced a $5.1 billion acquisition of AIG’s affordable housing assets. With over $12 billion in residential real estate investments announced in the past 60 days, Blackstone is back in a big way.

- In addition to Opendoor’s existing Agent Partner Program, it just announced a second Realtor referral program, Agent Access, which pays out a 1% referral fee plus bonuses ranging from $1,000 to $10,000 based on total number of referrals sent. Opendoor Partner Agents are not allowed to participate in Agent Access.

- On July 9, President Biden signed an executive order allowing occupational licensing across state lines and limiting noncompete agreements. While the order did not specifically mention real estate, the implications are significant. The growing number of Realtors nationwide and the many industry mergers and acquisitions could be impacted.

- Last Friday, Cloudstar, a data security provider and cloud-hosting company, fell victim to a sophisticated ransomware attack. Its 42,000 users including hundreds of title and escrow companies, currently do not have access to secure documents as everything was taken offline. The company is currently working with forensics experts and law enforcement as negotiations progress.

Final Thoughts:

Throughout the rest of the year, expect a further weakening of the seller’s market. The declining affordability and buyer fatigue combined with increased inventory are leading us towards a more normal, balanced market. When housing is more balanced, it is not quite as exciting, but it is much healthier and allows for long-term growth. It is time for the calm after the storm.

Copyright 2021 Sarah Perkins

Sarah Perkins is an award winning account executive and has been in title sales since 2004. As the Director of Industry Research & Senior Account Executive, Sarah’s role is to bring real estate transactions to Navi Title. Sarah supports her clients by helping them navigate the ever-changing real estate space through thorough research and understanding of current trends impacting today’s home buyers and sellers.

Leave a Reply